Aug 06 Challenger Report: Layoffs Fall, Hiring Picks Up; AI Leads For Fifth Straight Month

JULY LAYOFFS PLUNGE TO 33,429, HIRING PLANS TICK UP; AI LEADS REASONS FOR FIFTH CONSECUTIVE MONTH

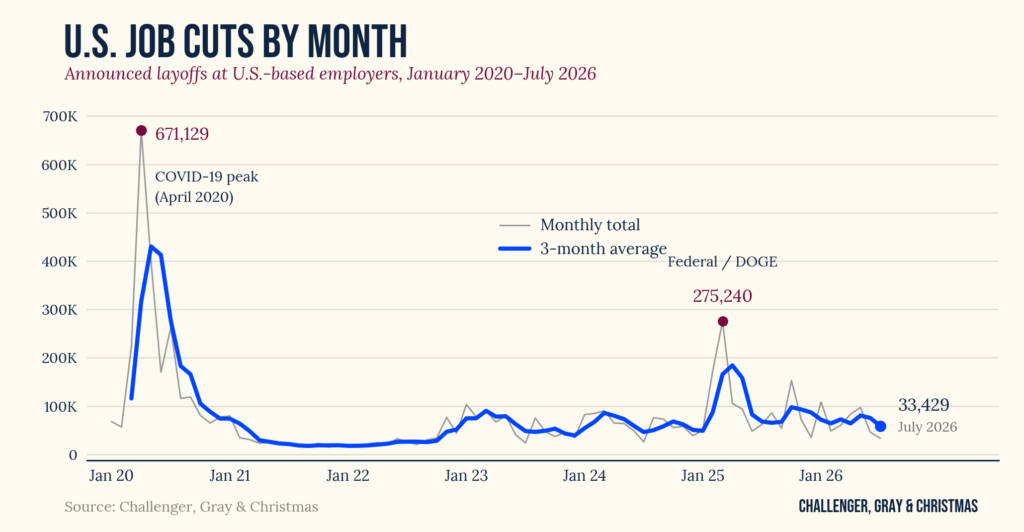

U.S.-based employers announced 33,429 job cuts in July, down 27% from the 45,849 cuts announced in June. It is down 46% from the 62,075 layoff plans announced in the same month last year, and marks the lowest monthly total in two years, according to a report released Thursday from global outplacement and executive coaching firm Challenger, Gray & Christmas.

July’s total is the lowest monthly total since July 2024, when 25,885 cuts were announced. Through July, employers have announced 477,033 job cuts, down 41% from the 806,383 cuts announced in the first seven months of 2025. It is the fifth time this year cuts are lower than the corresponding month one year earlier.

“The pace of layoffs fell dramatically this summer. Layoff plans continue to be announced primarily in Tech, and artificial intelligence is still the story, as investments in the technology reshape organizations.

“Hiring has also increased over last year by 25%, so while AI is shifting the labor market, it is not dismantling it,” said Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas.

WHICH INDUSTRIES CUT THE MOST IN JULY?

Technology again led all sectors, announcing 9,867 job cuts in July for a total of 149,023 in 2026. That is an increase of 67% from the 89,251 cuts announced in this sector through July 2025. Technology now accounts for 31% of all job cuts announced this year.

“Tech remains the center of gravity for this year’s cuts, and AI is still the reason companies give,” said Challenger.

Financial firms announced 3,157 cuts in July, the second-most of any industry, bringing the year-to-date total to 18,626. That is down 31% from the 26,894 cuts announced in this sector through July 2025.

Government announced 2,962 cuts in July for a year-to-date total of 20,752, down 93% from the 292,294 cuts announced through July 2025, when federal workforce reductions drove the year’s totals.

Services followed with 2,581 cuts in July, bringing the year-to-date total to 23,942. That is down 55% from the 53,438 cuts announced in this sector through July 2025.

Health Care companies and health products manufacturers, including hospitals, announced 1,251 cuts in July for a year-to-date total of 34,426, up 6% from the 32,399 cuts announced through July 2025.

Transportation has announced the second-most cuts among all industries this year with 41,748, up 303% from the 10,353 announced during the same period in 2025, as the sector continues to absorb elevated costs and shifting trade conditions.

The Media industry has announced 4,428 cuts so far in 2026, down 55% from the 9,796 cuts announced during the same period last year.

News, which Challenger tracks as a subset of Media and includes broadcast, digital, and print, has announced 1,311 cuts year-to-date, down 8% from the 1,418 News cuts announced through July 2025. July’s 273 was essentially flat from the same month last year, when 279 News cuts were recorded.

WHICH INDUSTRIES ARE CUTTING THE MOST IN 2026?

Technology leads all industries with 149,023 cuts announced through July, followed by Transportation with 41,748, Health Care/Products with 34,426, Services with 23,942, and Government with 20,752.

Eighteen of the 30 industries Challenger tracks have announced fewer cuts than they did at this point last year. The decline is steepest in Government, down 93%. Retail has announced 12,946 cuts, down 84% from 80,487. Warehousing is down 58% to 16,328.

The increases are concentrated in Technology, up 67%, Transportation, up 303%, and Pharmaceutical, up 312% to 13,666.

WHY ARE COMPANIES CUTTING?

In July, Artificial Intelligence (AI) led all reasons for job cuts, with 10,970 announced during the month, or 33%. It is the fifth consecutive month AI has been the leading reason. So far this year, AI has been cited in 112,713 job cut announcements, approximately 24% of all cuts.

Since 2023, when AI was first tracked as a distinct reason, it has been cited in 184,538 job cut announcements.

The ambiguous nature of what constitutes AI-attributed cuts was highlighted in July.

On the straightforward side, Visa announced a 7% reduction and attributed it to an efficiency push in which AI would reshape work. Challenger categorized those cuts as AI.

Challenger also tracked a Bronx hospital system, Montefiore, which eliminated 12 utilization review nursing positions after adopting software from Datavant. The New York State Nurses Association filed a class-action grievance and issued a press release in which it stated the hospital was replacing human workers with AI software. This would require the hospital to meet with union leaders under its new contract. However, the characterization is something hospital leaders refer to as “misleading” in a Gothamist article.

Datavant provides AI- and natural language processing-integrated software and highlights its AI tools on its website. However, since there was no clarity from the hospital system on the product being used, Challenger is tracking these cuts as “Technological Update (possibly AI).” Challenger uses this categorization when a company states new technology was the main reason for layoffs and AI is alluded to but not directly tied to the cuts. Challenger tracked 20,219 cuts for this reason in 2025.

“Naming AI in a layoff announcement can win over investors while pushing current and prospective employees away. That’s why the messaging has swung from hedging to aggressively citing it,” said Challenger.

“As regulations start to take shape, companies will be even more careful in their announcements, which would make tracking the impact of AI on jobs more opaque,” he added.

There is only one Health Care cut attributed to AI in Challenger’s data: 39 cuts at a California telehealth provider in October 2025.

“AI-related cutting has been limited outside of the Tech sector. Health Care is a place we do not expect many jobs to be displaced by AI, but one that has the potential to benefit from it and where AI is being used more and more often. If this software indeed runs on AI, this is an example of how AI is shifting and reshaping workplaces and also resulted in job loss,” said Challenger.

Market and Economic Conditions followed for the month with 7,960 cuts for a total of 90,075. Closings accounted for 6,060 in July and 84,630 for the year. Restructuring was cited for 2,815 cuts (57,476 through July 2026) and Loss of Contract for 2,003 (40,758 through July 2026).

HIRING PLANS IN 2026

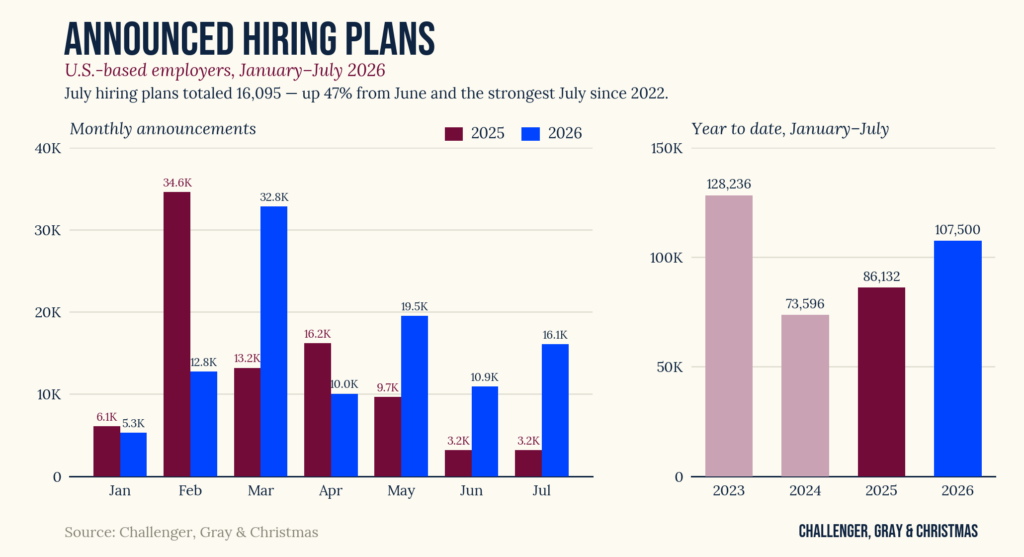

Employers announced plans to hire 16,095 workers in July, up 47% from the 10,933 plans announced in June and well above the 3,200 announced in July 2025. It is the highest July total since 2022, when employers announced 25,506 hiring plans.

So far this year, companies have announced plans to hire 107,500 workers, up 25% from the 86,132 plans announced through July 2025. It is the strongest January-to-July total since 2023.

Aerospace/Defense led all industries in July with 4,625 announced hires, followed by Technology with 2,470 and Automotive with 2,068. For the year, Technology leads with 17,231, followed by Automotive with 14,704 and Aerospace/Defense with 12,516.

“Employers are hiring more than they were at this point last year, which bucks the trend we’ve seen since 2020. The demand is showing up in aerospace, energy, and manufacturing, work that happens on a floor rather than a screen,” said Challenger.